In This Issue

Tax Tidbit

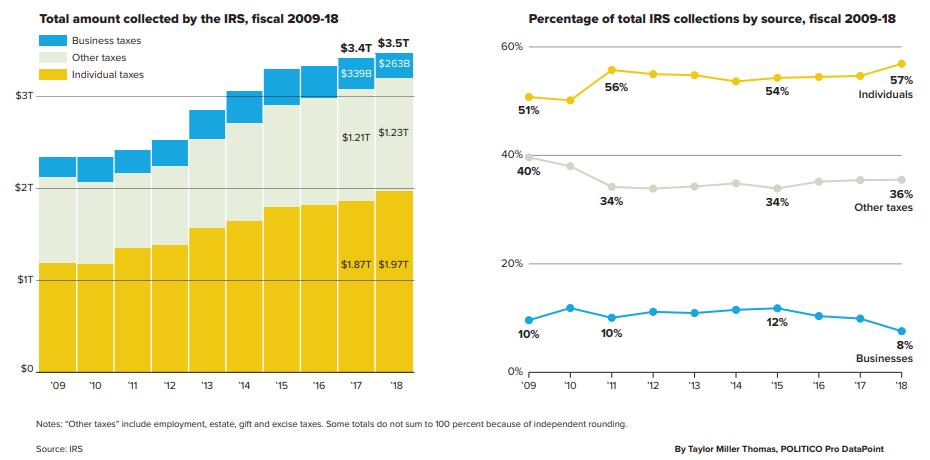

IRS By The Numbers. On May 20, the Internal Revenue Service (IRS) released its fiscal year 2018 Data Book, which provides an overview of the agency’s activities from Oct 1, 2017 to Sept. 30, 2018. Among other functions performed by the IRS, the Data Book provides insight into collections and refunds, penalties and criminal investigations, tax-exempt activities and the agency’s budget and workforce.

In the report detailing the sources of federal revenue collected in the most recent fiscal years, the agency received $1.97 trillion from individual taxes, a $10 billion increase from the previous year and a 3% jump from fiscal year 2015. Business collections, on the other hand, fell by 22% from $339 billion to $263 billion from the previous year—the third year in a row the measure has fallen.

The Tax Cuts and Jobs Act (P.L.115-97) lowered the corporate tax rate from 35% to 21% and made a number of changes to the individual tax rate, including a repeal of the personal and dependent exemptions, an expansion of the standard deduction and an increase in the child tax credit.

The report also shows the agency audited nearly 1 million, or 0.5%, of tax returns filed in 2017—about 100,000 less than the previous year and 500,000 fewer than in 2013. In addition, the IRS has seen a decrease of 15.5% decrease since 2013 in the number of full-time employees, which is currently 73,519. Treasury Assistant Secretary for Tax Policy David Kautter attributed the drop to technological advancements.

Legislative Lowdown

Stayin’ Alive. While lawmakers were back in their home districts for the district work period, staffers were hard at work in the Capitol trying to figure out the future of expired temporary tax provisions known as extenders. Last week, draft legislation was circulated among House Democratic offices that included a two-year extension of most expired tax extenders provisions, as well as increases to the Earned Income Tax Credit (EITC), the Child Tax Credit (CTC) and the Child and Dependent Care Tax Credit (CDTC). The bill’s changes to the EITC are expected to focus on increases for childless workers, and its edits to the CTC and the CDCTC may track closely with several bills recently introduced by Democrats, including Rep. Rosa DeLauro’s (D-CT) American Family Act (H.R.1560). To pay for these changes, Democrats may consider ending the TCJA reduction in the estate tax in 2023 instead of the provision’s current 2025 expiration date.

Apart from changes to the estate tax and increases to the EITC, CTC and CDCTC, the bill largely tracks with the Senate’s Tax Extender and Disaster Relief Act (S.617), which was introduced in February by Senate Finance Committee Chair Chuck Grassley (R-IA) and Ranking Member Ron Wyden (D-OR). Now that lawmakers are back in town, they are expected to move ahead with examining the temporary tax provisions in both the House and Senate. On the House side, the Ways and Means Committee will determine which extenders to keep and which to discard. On the Senate side, the Finance Committee task forces established before Memorial Day will begin to explore long-term solutions to extenders. If the final House legislation tracks closely with what is currently in the draft legislation, the bill is unlikely to be endorsed by Senate Republicans.

To TCJA, or Not to TCJA? While Republicans have highlighted the 2017 Tax Cuts and Jobs Act (P.L. 115-97) (TCJA) as a force spurring the U.S. economy and record-low unemployment rates, the nonpartisan Congressional Research Service (CRS) pulled out their calculators on May 22. Specifically, the report claimed “relatively small” first-year effects on the economy and “very little growth in wage rates” for ordinary workers as a result of the cut. Despite identifying an increase in business investment and GDP growth, the report noted that both indicators were on par with previous estimates and trends before the tax cuts. The report further confirmed that the benefits of the significantly reduced corporate tax rate ultimately went to stock buybacks to the tune of $1 trillion, indicating that the returns on capital and labor investment were relatively less attractive to the biggest U.S. companies. Encouragingly, the report did highlight a multinational repatriation windfall of $664 billion in 2018 as a result of the tax changes, nearly four times as much as in past years. Several analysts from think tanks, including Brian Riedl of the Manhattan Institute noted that the CRS downplayed the TCJA’s impact on the economy, which spiked up to 3% even in its ninth year of expansion. Riedl noted that the TCJA is responsible for the spike this far into an economic expansion. Of course, the report has already emboldened accusations by Democrats that the economic growth promised by TCJA was overstated and ultimately fiscally burdensome in the long-run. Republicans will continue to point to delayed effects of the tax cuts and underscore the record-low unemployment rate and consistent job growth.

The Retirement Exchange. Before Congress left town for the Memorial Day work period, senators were busy passing legislation to fix a provision in the Tax Cuts and Jobs Act (P.L.115-97) that unintentionally raised taxes on Gold Star families. The bill, the Gold Star Family Tax Relief Act (S.1370)—which passed the upper chamber under unanimous consent—would ensure that benefits received by the children of slain heroes would be treated as earned income of the children, effectively exempting the benefits from taxes.

Across the capitol, the House passed with overwhelming bipartisan support the Setting Every Community Up for Retirement Enhancement (SECURE) Act (H.R.1994) along a 417-3 vote. In a last-minute wheel and deal, a provision that would have expanded 529 education accounts to include homeschooling costs was removed in exchange for the Gold Star family provision. Quickly after the bill cleared the House, there was chatter it might be approved under unanimous consent in the Senate—meaning if no senator objected, the bill would be sent to President Trump for his signature. However, that effort was cut short when Sen. Ted Cruz (R-TX) decided to block the measure over concerns that the House bill removed expansions to 529 provisions allowing plan funds to be used for homeschooling expenses, which is something he has championed over the years.

Mnuchin’s Special Measures. In a May 23 letter to congressional leadership and the top Republicans and Democrats on the House Ways and Means Committee and the Senate Finance Committee, Treasury Secretary Steven Mnuchin notified lawmakers that the statutory debt limit has made him unable to fully invest funds from the Civil Service Retirement and Disability Fund not immediately required to pay beneficiaries. Because of this, the “debt issuance suspension period” that originally was to end on June 5 will now continue through July 25. Mnuchin noted that given the number of unknown factors, the “effective duration of the extraordinary measures is subject to considerable uncertainty.” Despite the uncertainty, he expects the extraordinary measures to be exhausted by late summer. Mnuchin urged lawmakers to increase or suspend the statutory debt limit as soon as possible.

Build that Bureau. On May 22, the House passed the Consumers First Act (H.R. 1500) along a 231 to 191 vote. The legislation is aimed at strengthening and reinstating programs at the Consumer Financial Protection Bureau (CFPB) that were weakened under the deregulatory regime of the agency’s previous director, Mick Mulvaney. Specifically, the bill would restore previous supervisory and enforcement authorities for the Office of Fair Lending and under the Military Lending Act, while additionally reinstating the Consumer Advisory Board and the student loan office. However, considering that the bill passed the House along a purely partisan vote, the House-passed bill will almost certainly not be considered in the Senate, and would face long odds of passage if separately introduced in the Senate.

RegWatch

Guidance Game Plan. The Internal Revenue Service (IRS) outlined the timeframe under which it anticipates releasing guidance on the provisions included within the Tax Cuts and Jobs Act (P.L.115-97). According to a 10,000-row spreadsheet obtained by Tax Notes through a Freedom of Information Act disclosure, the IRS has already missed some of its target dates to issue guidance. Below are some target dates the IRS outlined for releasing final regulations on the following provisions:

- Foreign Tax Credit: June 21

- Deduction related to the foreign-derived intangible income (FDII): July 31

- Global Intangible Low-Taxed Income (GILTI): July 31

- Base Erosion Anti-abuse Tax (BEAT): August 16

- Hybrid Transactions and Hybrid Entities: September 23

The IRS outlined the following dates for proposed regulations:

- Definition of Previously Taxed Earnings and Profits: August 16. As of Feb. 26, the green circulation for those rules was already completed, but the pink circulation had not yet begun

- Deduction for Dividends Received from Foreign Corporations (Sec.245A): March 29—with a June 21 target for final regulations.

- Special rules concerning the participation exemption system for the taxation of foreign-source income follow the same timeline: March 29—with a June 21 target for final regulations.

It is unclear whether the IRS will be able to meet all its deadlines. The IRS has until June 22 to issue guidance that can be retroactively applied to the enactment of the TCJA on Dec. 22, 2017. The full timeline of regulations is below.

Repatriation Guidance Leads to Overpayments. According to a May 22 report from the Treasury Inspector General for Tax Administration (TIGTA), at least 115 corporations unintentionally overpaid $2.8 billion to the Internal Revenue Service (IRS) through their attempts to comply with Section 965 repatriation guidance. The Tax Cuts and Jobs Act (P.L.115-97) provides for a one-time deemed repatriation tax on foreign earnings, but the report blames the lack of guidance for the overpayment. The IRS said it is unable to issue any refunds until the entire Section 965 liability is paid, and TIGTA recommended that in this case, the IRS should inform corporations of their liability status, including when their next payment is due. The IRS agreed with TIGTA’s recommendations.

The Settlement to End All Settlements. The Office of the Comptroller of the Currency (OCC) and Federal Deposit Insurance Corporation (FDIC) reached a settlement with a payday lenders association over ongoing issues to the “Operation Choke Point” regulations. The settlement, expected to proceed as soon as senior FDIC officials review and approve of the federal court filing, would effectively resolve ongoing accusations by the Community Financial Services Association of America that leading financial regulators had pressured banks to block out payday lenders under the rule’s mandates. With the claims against the FDIC being dropped, the agency will reportedly issue a statement describing its internal processes for determining how a bank could eliminate a customer’s deposit account; meanwhile, allegations against the OCC would be dropped as a result of the resolution.

1111 Constitution Avenue

TIGTA Releases Semiannual report to Congress. The Treasury Inspector General For Tax Administration (TIGTA) released its semiannual report to Congress yesterday in which it explained its efforts to audit the Internal Revenue Service’s (IRS) implementation of the Tax Cuts and Jobs Act (P.L.115-97) and its attempts to secure sensitive taxpayer data. In the report, TIGTA announced its Office of Audit conducted 20 audits and its Office of Investigations completed 1,608 investigations, which led to the recovery, protection and identification of $1.4 billion.

Regarding the rollout of TCJA guidance, the report specifically highlights the implementation of the Sec. 199A Qualified Business Income Deduction provision, saying “a separate tax form would allow the IRS to capture data to assist in evaluating compliance with the deduction requirements. The IRS could use information from a form to improve systemic identification of erroneous deduction amounts.” On the security front, TIGTA explained that it identified more than 652,000 fraudulent returns, preventing more than $7.2 billion in fraudulent refunds.

Section 956 Guidance. On May 22, the Internal Revenue Service (IRS) and Department of the Treasury released final regulations that reduce the amount determined under section 956 for domestic corporations that are U.S. shareholders to the extent that, such shareholders would be allowed a deduction under section 245A (the dividends-received-deduction.) The regulations are adopted with modifications from proposed regulations (REG-114540-18) that were issued in November of last year. The regulations affect certain domestic corporations that own (or are treated as owning) stock in foreign corporations. The regulations will be effective on July 22, 2019.

Updated W-4 Form. On Friday, the Treasury Department released its new W-4 form, which includes a five-step process—three of which are optional—that allows taxpayers to calculate the tax withheld from their paychecks. The agency has been working to develop a new version of the form that reflects tax law changes that went into effect last year after the passage of the Tax Cuts and Jobs Act (P.L. 115-97). The new form provides taxpayers with more than one job information on how to calculate income not subject to withholding. In response to the new form, Internal Revenue Service Commissioner Chuck Rettig said "the primary goals of the new design are to provide simplicity, accuracy and privacy for employees while minimizing burden for employers and payroll processors." A draft was released last June but was quickly scrapped after tax professionals deemed it too complicated and expressed concerns that it would lead to under-withholding. The form released on Friday is only a draft, and the Treasury Department intends to produce a final version by the end of the year. The new form will not be effective until 2020.

At a Glance

- Art of the Curve. Art Laffer, creator of the economic theory positing that tax revenue can be optimized at a certain tax rate, will receive the Presidential Medal of Freedom, the White House announced. Republicans have long pointed to the “Laffer Curve” in support of their push for tax cuts, arguing their policies can spur economic growth while simultaneously raising government revenues.

- Hassett Hangs His Hat. Kevin Hassett, Chairman of the White House Council of Economic Advisers, announced his imminent departure Sunday night. Formerly of the American Enterprise Institute, among his many responsibilities he also worked closely on the president’s immigration plan, and on Monday Hassett refuted claims that he is parting with the administration over Trump’s threats to impose tariffs on Mexican goods should that nation fail to comply with the new U.S. plan. Hassett advocated for the positive impacts of immigration and free trade prior to joining the Trump economic team.

- You’re Hot then You’re Cold. Treasury Department nominees advancing to a full Senate vote face a hold by Sen. Ron Wyden (D-OR). The Senate Finance Committee top Democrat threatened to freeze the proceedings until the agency cooperates with Ways and Means Chair Richard Neal’s (D-MA) request for six years of President Trump’s personal tax returns. In response, the Treasury Department called Neal’s request “categorically different” from previous Congressional requests for presidential tax returns, and said it raised “serious constitutional questions.”

- And To All a Good Knight. In late May, Shahira Knight, a veteran of the House Ways and Means and the Joint Economic Committees, announced her intent to leave her post as President Trump’s legislative affairs director. The high-level departure comes as the administration is in the midst of ongoing negotiations to craft a replacement for the North American Trade Agreement (NAFTA) and to increase the debt ceiling.

- A Boost for Congressional Coffers? This weekend, House Democrats announced an appropriations bill that would increase discretionary funds (by $1.4b), raise funding to Treasury (by $793.9m), and IRS (by $697.4m), and also increase civilian federal employee pay (by 3.1%). The bill does not include any provision to block an automatic pay raise for members of Congress; the automatic raise would be the first since 2009. Evan Hollander, a spokesman for the House Appropriations Committee, indicated any changes to the automatic pay will stem from the authorizing process.

- Tax Nomination Takes Flight. On May 23, Emin Toro, nominee for U.S. Tax Court Judge, cleared the Senate Finance Committee on a 28-0 vote. Toro, currently a partner at Covington & Burling and formerly a law clerk for Supreme Court Justice Clarence Thomas, now advances to a full chamber vote before he can claim a seat on the bench.

Brownstein Bookshelf

- Opportunity Zones. Brownstein’s Nicole Ament analyzes pathways for interested investors to engage in the opportunity zones regulations produced by the Tax Cuts and Jobs Act (P.L.115-97).

- No, Really, Opportunity Zones. Not to be outdone, Sarah Walters from Brownstein’s Energy Environment and Resource Management (EERS) team wrote how tribes can take advantage of the opportunity zones regulations to spur business in reservation communities.

- Brower Knows. Watch Greg Brower from our D.C. office discuss a federal judge’s ruling regarding access to the president’s financial records and ongoing revelations following the Mueller investigation. Watch him here or here on CNN, or here four days later on MSNBC. (He’s on TV a lot).

Regulation Station

INTERNATIONAL

|

Regulation

|

Latest Action

|

Regulation Link

|

Comment Countdown

|

Brownstein Commentary

|

|

Sec. 956

|

May 23, 2019

Final Regulations

|

2019-10749

|

N/A

|

|

|

Sec. 965

Transition Tax

Correction

|

April 10, 2019

|

2019-07012

2019-07018

|

N/A

|

|

|

FDII and GILTI

|

March 6, 2019

|

REG-104464-18

|

Deadline Passed

May 6, 2019

|

|

|

Sec. 965

Transition Tax

|

Feb. 5, 2019

Final Regulations

|

84 FR 1838

|

Deadline Passed

Oct. 9, 2018

|

|

|

Certain Hybrid Arrangements

|

Dec. 28, 2018

|

REG-104352-18

|

Deadline Passed Feb. 26, 2019

|

|

|

BEAT (Sec. 59A)

|

Dec. 21, 2018

|

REG-104259-18

|

Deadline Passed Feb. 19, 2019

|

|

|

Foreign Tax Credit

|

Dec. 7, 2018

|

REG-105600-18

|

Deadline Passed

Feb. 5, 2019

|

|

|

Sec. 956

|

Nov. 5, 2018

|

REG-114540-18

|

Deadline Passed Dec. 5, 2019

|

|

|

GILTI

|

Oct. 10, 2018

|

REG-104390-18

|

Deadline Passed

Nov. 26, 2018

|

|

|

GILTI

|

Sept. 13, 2018

|

Rev. Proc. 2018-48

|

N/A

|

|

199A

|

Regulation

|

Latest Action

|

Regulation Link

|

Comment Countdown

|

Brownstein Commentary

|

|

Qualified Business Income Deduction (Sec. 199A) - CORRECTION

|

April 17, 2019

|

84 FR 15953

|

N/A

|

|

|

Qualified Business Income Deduction (Sec. 199A)

|

Feb. 8, 2018

|

REG-134652-18

|

Deadline Passed

April 9, 2019

|

|

|

Qualified Business Income Deduction

(Sec. 199A)

|

Feb. 8, 2019

Final Regulations

|

84 FR 2952

|

Deadline Passed

Oct. 1, 2018

|

|

|

W-2 Wages for Qualified Business Income Deduction

(Sec. 199A)

|

Jan. 18, 2019

|

Rev. Proc. 2019-11

|

N/A

|

|

|

Trade or Business Safe Harbor: Rental Real Estate

(Sec. 199A)

|

Jan. 18, 2019

|

Notice 2019-07

|

N/A

|

Washington Update

|

DOMESTIC BUSINESS

|

Regulation

|

Latest Action

|

Regulation Link

|

Comment Countdown

|

Brownstein Commentary

|

|

Interest Expense Deduction

|

Dec. 28, 2018

|

REG-106089-18

|

Deadline Passed Feb. 26, 2019

|

|

|

Opportunity Zones

|

Oct. 29, 2018

|

REG-115420-18

|

Deadline Passed

Dec. 28, 2018

|

|

|

Debt-Equity Documentation

(Sec. 385)

|

Sept. 24, 2018

|

REG-130244-17

|

Deadline Passed

Dec. 24, 2018

|

|

|

Sec. 162(m)

|

Aug. 21, 2018

|

Notice 2018-68

|

N/A

|

Washington Update

|

|

Full Expensing

|

Aug. 3, 2018

|

REG-104397-18

|

Deadline Passed

Oct. 9, 2018

|

|

|

Carried Interest

|

March 1, 2018

|

Notice 2018-18

|

N/A

|

|

EXEMPT ORGANIZATIONS

|

Regulation

|

Latest Action

|

Regulation Link

|

Comment Countdown

|

Brownstein Commentary

|

|

Excise Tax on Executive Compensation

|

Dec. 31, 2018

|

Notice 2019-09

|

N/A

|

|

|

UBIT (Sec. 512(a)(7))

|

Dec. 10, 2018

|

Notice 2018-99

|

N/A

|

|

|

Time and manner for filing and paying excise taxes

|

Nov. 7, 2018

|

REG-107163-18

|

Deadline Passed

Dec. 7, 2018

|

|

|

UBIT (Sec. 512(a)(6))

|

Aug. 21, 2018

|

Notice 2018-67

|

N/A

|

Washington Update

|

|

Higher Education Excise Tax

|

June 8, 2018

|

Notice 2018-55

|

Deadline Passed

Sept. 6, 2018

|

|

OTHER

This document is intended to provide you with general information regarding {{DISCLAIMER_TEXT}}. The contents of this document are not intended to provide specific legal advice. If you have any questions about the contents of this document or if you need legal advice as to an issue, please contact the attorneys listed or your regular Brownstein Hyatt Farber Schreck, LLP attorney. This communication may be considered advertising in some jurisdictions.