28th Time’s the Charm?

For 27 years in a row Congress has failed to pass its 12 spending bills by the Sept. 30 deadline. Will this year bring more of the same? Or will the streak finally be broken?

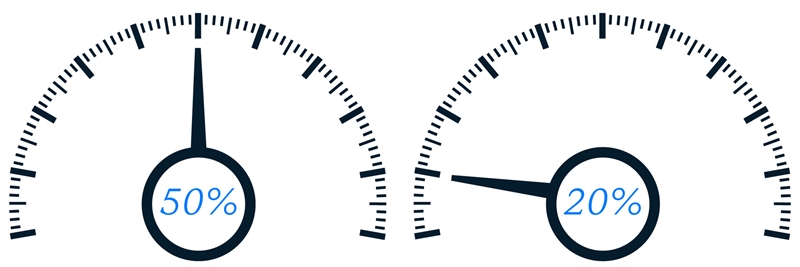

Russ-O-Meter

Estimates on tax policy questions from shareholder Russ Sullivan

| What are the Chances of a Year-End Tax Package? | What are the Chances of a Government Shutdown in September? |

Short-Term CR to Avert a Government Shutdown Likely in September

With only 11 legislative days left before the Sept. 30 fiscal year deadline, Congress is unlikely to pass anything other than a short-term continuing resolution (CR). The House Appropriations Committee approved 10 of the annual appropriations bills, though the full chamber has voted to pass only one of the bills (Military Construction-Veterans Affairs). The Senate Appropriations Committee has approved all 12 annual appropriations bills, though none of these bills has advanced through the full Senate. Additionally, there is a $115 billion difference between the two chambers’ appropriations bills, which will need to be addressed in a final deal.

The best we can hope for by Sept. 30 is a short-term CR that goes through the end of November or early December. This will give Congress much-needed time to strike a potential deal. The chances of a shutdown after the expiration of a short-term CR are much higher.

Year-End Tax Package

Lawmakers on both sides of the aisle have been working toward a tax deal for over a year. With key provisions of the Tax Cuts and Jobs Act of 2017 either having expired or soon expiring, lawmakers are eager to strike a deal. However, a potential package hinges on whether Democrats and Republicans can agree to an extension and expansion of the child tax credit (CTC) to balance the extension of several business-related provisions, with a focus on the research and development (R&D) amortization deduction, bonus depreciation, and the net business interest deduction:

- R&D Amortization: Historically, taxpayers were permitted to deduct certain research and development (R&D) costs immediately under section 174. However, beginning in 2022, businesses must amortize R&D expenditures over five years. Lawmakers have introduced bipartisan proposals to reverse the restrictions retroactively, although those have failed to be enacted despite growing industry concerns about the impact of the amortization requirement, especially on startup enterprises.

- Accelerated Bonus Depreciation: Through 2022, taxpayers could claim the 100% bonus depreciation under section 168(k) for eligible property placed in service during the taxable year. However, starting this year, the bonus-depreciation allowance is 80%, the first step in a phase down by 20% annually until it is entirely eliminated for equipment placed in service after 2026.

- Business Interest Limitation: Through 2021, the deduction for net business interest expense under 163(j) was limited to a maximum of 30% of a taxpayer’s earnings before interest, taxes, depreciation and amortization (EBITDA). Beginning in 2022, the provision narrowed to allow the deduction based on only earnings before interest and taxes (EBIT)—not taking into account depreciation or amortization.

These three provisions were included in the Republican Ways and Means Committee’s comprehensive tax package (H.R. 3936, H.R. 3937 and H.R. 3938). While two of the three provisions have bipartisan support, Democrats in both chambers have indicated that they also want support for working families in any legislation that addresses expired business provisions—most likely an expansion of the CTC.

Ways and Means Committee Chairman Jason Smith (R-MO) is a strong advocate for extending the increased CTC enacted in TCJA, and he previously introduced legislation to make permanent the $2,000 per-child credit amount. Democrats would like to see the credit restored to levels enacted under the Democrats’ 2021 Reconciliation bill, the American Rescue Plan Act (ARPA), which increased the value of the credit for $3,600 for children age 5 and under and $3,000 for children age 6 and over. That credit was also available in monthly installments. A possible CTC deal would need to find the middle ground between the Democratic and Republican proposals. It would also likely have to be paired with some form of a continuation of work requirements under current law—a stipulation that Sen. Joe Manchin (D-WV) insisted on throughout negotiations over a potential CTC provision in the Democrats’ Fiscal Year 2022 reconciliation bill, the Inflation Reduction Act.

In addition to these priorities, U.S. auto dealers may finally see some success in their ongoing effort to seek broad relief for an elective deferral of last-in, first-out (LIFO) accounting provisions. Last year, on Dec. 23, the Senate passed the Supply Chain Disruptions Relief Act, a bill led by Sen. Sherrod Brown (D-OH) that would allow auto dealers to wait until 2025 to replace their inventory. However, the bill was unable to pass the House due to procedural rules concerning the origination of tax bills. With broad bipartisan support, this provision could also be included in a year-end tax package.

Additionally, a solution on 1099-K reporting may also be included. The reporting threshold for third-party payment platforms to issue a Form 1099-K decreased from $20,000 and 200 transactions to $600 in 2023—this change was enacted pursuant to ARPA. While the change was intended to increase the number of transactions subject to reporting, it attracted criticism from certain lawmakers who argued the lower threshold imposes an undue administrative burden. Negotiations are ongoing on what an appropriate threshold might be

For more information on the ongoing negotiations into both a potential year-end tax bill and the IRS’s budget, the Brownstein National Tax Policy Group recently recorded a podcast where members of the Tax Team shared their insights into the topography of the tax landscape. The podcast is available here.

Legislative Lowdown

Lawmakers Prepare for IRS Funding Fight. Lawmakers returned to Capitol Hill on Sept. 5 after a monthlong congressional recess with an eye on the 12 Fiscal Year 2024 appropriations bills that must pass before Oct. 1 to avoid a government shutdown, in the absence of a continuing resolution (CR). Many of the appropriations bills, especially those advanced by the Republican-controlled House Appropriations Committee, contain clawbacks to either funding for the IRS contained within the Inflation Reduction Act (IRA, Pub. L. 117-169) or to the IRS’s annual enforcement and operations support budget appropriated every fiscal year. These appropriations bills are set up for a collision course with Senate Democrats’ appropriations bills, which keeps funding for the agency flat.

Although President Biden and House Speaker Kevin McCarthy (R-CA) have informally agreed to a $10 billion IRS-IRA funding clawback for Fiscal Year 2024, many Republican appropriations bills exceed this amount.

Below are the House appropriations bills containing IRS clawbacks:

Financial Services and General Government (FSGG) Bill: The House FSGG spending bill would freeze spending for taxpayer services and operations support at FY2023 amounts, while proposing a significant $1.2 billion (22%) cut to tax enforcement. The bill would restore funding to the business-systems modernization account, providing $150 million to supplement the $4.75 billion in funding allocated for this task by the IRA. Additionally, the proposed House FSGG bill would rescind approximately $10.2 billion of the supplemental funding provided to the IRS by the IRA. The bill proposes repealing $6.1 billion of the funding allocated specifically for enforcement and $4.1 billion of the funding allocated for operations support. The bill also includes a provision to prevent the IRS from using any funding to develop or provide taxpayers with a “free, public electronic return-filing service option” without prior approval from both the House and Senate Appropriations committees and tax-writing committees.

In contrast, the Senate Appropriations Committee reported its FSGG bill favorably on July 13 by a unanimous 29-0 vote. The bill would hold IRS spending levels flat at approximately FY2023 amounts and would rescind $10 billion in enforcement from IRA-provided IRS funds—the same amount agreed to by Biden and McCarthy.

Transportation, Housing and Urban Development and Related Agencies (THUD) Bill: The House THUD spending bill would rescind about $25 billion of the IRA’s unobligated tax-enforcement funding.

Commerce, Justice, Science and Related Agencies (CJS) Bill: The House Appropriations CJS Subcommittee’s spending bill would rescind about $12.9 billion and $9.1 billion from the IRA’s unobligated tax-enforcement and operations-support funding for the IRS, respectively.

Labor, Health and Human Services, Education and Related Agencies (LHHS) Bill: The House Appropriations LHHS Subcommittee’s spending bill would rescind about $9.8 billion of the IRA’s unobligated operations-support funding for the IRS.

Democratic Lawmakers Accuse Tax Preparers of Fighting Direct e-File While Advocacy Group Begins Messaging Campaign. Sen. Elizabeth Warren (D-MA) and Rep. Katie Porter (D-CA) sent letters to tax-preparation companies and industry trade groups on Aug. 23 requesting information on their efforts to lobby the government against the creation of an IRS-operated Direct e-File option. The lawmakers addressed the four letters to the heads of Intuit, H&R Block, the Free File Alliance and the American Coalition for Taxpayer Rights. Much of the information sought is publicly available. The letters accused the recipients of launching a “lobbying campaign aimed at protecting [their] ability to gouge taxpayers and preventing the creation of a free and simple system for taxpayers to file their taxes.” The recipients of the letter acknowledge that they are exercising their First Amendment rights.

Free File Alliance Executive Director Tim Hugo responded to the letter on Aug. 25. Hugo noted that a simple and free system for taxpayers to file their taxes already exists via the Free File program. Hugo also pointed to a recommendation included in a recent Electronic Tax Administration Advisory Committee report that offered support for expanding existing free-file programs before investing agency funds into the creation of a new IRS-operated system. An Intuit spokesperson also issued a response on behalf of the company, arguing that the Direct e-File effort “is a solution in search of a problem, and that solution will unnecessarily cost taxpayers billions of dollars.”

On Aug. 14, the Coalition for Free and Fair Filing (CFFF) hosted a webinar with Sen. Warren and Rep. Porter, along with Rep. Don Beyer (D-VA), to highlight support for the 2024 Direct e-File Pilot. The members spoke in support of the organization’s efforts, criticizing paid preparers and tax-preparation software companies for their opposition to the IRS’s development of the platform. Warren and Porter shared sentiments reflected in their earlier letters, and all three members disparaged the Free File program for not providing reliable services for low-income Americans.

Over the past two decades, the Free File Program has helped file over 70 million free federal and state income tax returns, in addition to what individual companies provide as a pro bono service. Additionally, the IRS Volunteer Income Tax Assistance program serves low-income individuals that have earnings below a certain threshold.

Tax Worldview

Ways and Means Republicans Take Opposition to OECD Two-Pillar Plan Abroad. On July 30, House Ways and Means Committee Chairman Jason Smith (R-MO) led a bipartisan delegation of House members to Seoul, South Korea. Among other topics, the delegation discussed South Korea’s decision of delaying the implementation of its undertaxed profits rule (UTPR), a critical facet of the Organisation for Economic Co-Operation and Development’s (OECD) Pillar Two global minimum-tax regime that Ways and Means Committee Republicans have uniformly opposed. After having discussions with South Korean President Yoon Suk Yeol and other South Korean government officials, Chairman Smith expressed approval for South Korea’s decision to delay its UTPR but stressed that “Congress will not tolerate foreign taxes on U.S. operations of U.S. businesses because such taxes violate our sovereignty and harm American workers.”

Chairman Smith and seven of his Republican Ways and Means Committee colleagues went to discuss the OECD global minimum-tax (GMT) regime by visiting OECD officials in Paris on Sept. 1. Chairman Smith and his colleagues reiterated that they believe the deal would negatively affect U.S. interests and that the Treasury Department unconstitutionally sidestepped congressional authority by negotiating U.S. tax policy with the OECD. Noting the United States’ current global minimum-tax scheme, the global intangible low-taxed income (GILTI) tax, Chairman Smith warned that international adoption of a UTPR will lead Congress to “aggressively pursue tax and trade countermeasures.” The delegation also criticized the “disjointed” and “discriminatory” digital service taxes that, if retained with the adoption of Pillar One, would create double taxation that would disproportionately affect U.S. companies. Reps. Randy Feenstra (R-IA) and Nicole Malliotakis (R-NY) also raised concerns about how China’s refundable research and development (R&D) tax credit payments would be treated favorably under the Pillar Two global minimum tax, while American nonrefundable R&D credits would count against U.S. multinational companies, thereby putting them at a competitive disadvantage.

Lastly, Chairman Smith and other Ways and Means Committee Republicans visited Berlin to discuss the OECD provisions with top German finance officials on Sept. 5, echoing many of the comments the delegation made in Paris. Chairman Smith also expressed his willingness to engage in retaliatory measures should the pillars be adopted, saying, “if [the] global minimum tax [is] passed in other countries, it’s going to create great [economic] instability … because our committee will move forward with Tax and Trade mechanisms to make sure that we are making whole our companies that are being targeted by other countries.”

The delegation also used the opportunity to raise concerns about Germany’s imposition of its 1925 withholding tax—so-called Section 49—on income from German-registered intellectual property of nonresident companies, previewed in a letter to German Finance Minister Christian Linder on Aug. 29. Their concerns echo a prior letter from eight Ways and Means Committee Republicans to Treasury Secretary Janet Yellen on June 8 asking for her assistance in resolving the matter, which stakeholders view as a discriminatory and extraterritorial tax on U.S. companies.

Canada Previews Digital Services Tax. On Aug. 4, Canada unveiled draft legislation to implement a digital services tax (DST) to take effect starting in 2024, despite an agreement among countries promoting the OECD two pillar global tax regime to delay any implementation of DSTs until 2025. The proposed Canadian tax would affect global entities that earn digital services revenue through online marketplace, advertising, social media or user data services, detailed in 138 pages of explanatory notes. Canada staked out its contrary position due to continuous delays from the OECD’s governing body on its planned enactment date for the provisions. In a July statement, Canadian Deputy Prime Minister and Minister of Finance Chrystia Freeland said that while they continue to be open to a multinational treaty and remain supportive of continued OECD negotiations, “Canada cannot support the extended standstill” of implementation and that “it is really important for us to defend our national interest” with regard to collecting digital services tax revenue.

Canada’s decision has been heavily criticized by U.S. officials and business groups like the National Foreign Trade Council, calling it “clearly discriminatory toward U.S. companies” and potentially foreshadowing other countries to maintain suspended DSTs that disproportionately affect U.S. companies. Biden administration officials have called on Canada to reconsider its DST position, and some have considered implementing retaliatory measures against Canada should its DST come into effect.

Developing Countries Urge United Nations Engagement on Global Minimum Tax. A number of developing countries have raised concerns that the OECD’s two-pillar system does not treat them fairly. Their perspective is shared by United Nations (UN) Secretary-General António Guterres, who released an advance unedited version of a report on Aug. 8 criticizing the OECD for failing to take the needs of developing nations into account in the OECD two-pillar framework. Guterres’ report calls for more UN involvement in drafting and setting global tax rules, to prevent developed countries from implementing rules that disproportionately affect poorer member states. The report also puts the OECD and UN at odds with each other as they fight for leadership in setting global tax policy. OECD staff disapproved of the “surprising” UN report, stating that the UN was ignoring the progress the OECD has made in successfully developing equitable economic policy over the last two decades.

1111 Constitution Ave.

IRS Announces Effort to Utilize IRA Funding to Conduct Tax Enforcement on High-Income Earners. On Sept. 8, the IRS issued Notice 2023-166 stating that it would shift tax-enforcement efforts away from low- and middle-income individual taxpayers in favor of increased scrutiny of high-income earners, corporations and partnerships. The agency says that it has been able to make this shift due to funding from the Inflation Reduction Act (IRA, Pub. L. 117-169). A more expansive explanation of what mechanisms the IRS intends to use will be announced in the coming weeks and months, but the notice notably included that artificial intelligence technology will be leveraged to identify high-risk tax issues present in large and complex partnership structures. Senate Finance Committee Chairman Ron Wyden (D-OR) praised the announcement, stating, “I’m pleased to see the IRS using the enforcement funding from the Inflation Reduction Act to crack down on large, complex partnerships using ground-breaking technology—this … represents a fresh approach to taking on sophisticated tax cheats.” Meanwhile, House Ways and Means Committee Chairman Jason Smith (R-MO) stated that the announcement does not provide adequate details of how the agency plans to “shield” taxpayers earning less than $400,000 per year from audits, and that prior similar announcements were “just thinly veiled confirmations of more audits” for middle-class families.

After Congressional Inquiry on Missing Digital-Asset Reporting Guidance, Treasury and IRS Release Proposed Regulations. Four Democratic senators sent a letter to Treasury Secretary Janet Yellen and IRS Commissioner Daniel Werfel on Aug. 2 to request an update on regulators’ progress in developing updated reporting requirements for digital-asset brokers. The lawmakers, led by Sen. Elizabeth Warren (D-MA), recommended urgency in implementing these regulations, highlighting that “[r]esearch suggests that crypto tax evaders are cheating the IRS out of at least $50 billion a year.” The amended reporting requirements are intended to compel certain third-party brokers to report information with respect to the sales, gains and losses attributed to cryptocurrencies and other digital assets to the federal government. The letter noted that regulators have not yet released initial proposed rules for brokers despite a mandate included in the Infrastructure Investment and Jobs Act (IIJA, Pub. L. 117-58) to issue final reporting regulations by Jan. 1, 2024.

The Treasury Department and IRS subsequently issued proposed regulations (RIN 1545-BP71) on Aug. 25 providing new reporting requirements for digital-asset brokers, including those catering to users engaging in the sale or exchange of cryptocurrencies and nonfungible tokens. The guidance implements a provision enacted in the IIJA designed to increase taxpayer compliance in the digital-asset space by requiring cryptocurrency exchanges like Binance and Coinbase to report certain sales and provide forms to customers with respect to digital-asset transactions. The guidance also implements new broker-to-broker reporting requirements and mandates that business transactions of more than $10,000 in value be reported to the IRS. The Treasury Department and IRS proposed a new reporting document (Form 1099-DA) to assist taxpayers in complying with the new requirements.

The proposed regulations exempt cryptocurrency miners from reporting requirements unless they conduct transactions. Although the IIJA mandated that the rules apply beginning in 2024, the Treasury Department and IRS suggested that the proposed regulations be delayed until 2025 to provide time for regulators to consider public comments on the guidance and for exchanges to modify processes to adhere to the final rules once they are released. The delay was praised by cryptocurrency exchanges, who noted that it would help them improve compliance but was criticized by some Democratic lawmakers who believed that it will further increase the tax gap. At the time the IIJA was passed, the Joint Committee on Taxation estimated that the new rules would reduce the federal deficit by $28 billion over a decade.

House Financial Services Committee Chair Patrick McHenry (R-NC) denounced the guidance proposal as “another front in the Biden administration’s ongoing attack on the digital-asset ecosystem.” He claimed that lawmakers agreed in the IIJA that rules must be “narrow, tailored, and clear” and “adhere to Congressional intent,” which he says the proposed regulations fail to do. The Treasury Department and the IRS have scheduled a public hearing on Nov. 7 to solicit oral feedback, and written comments can be submitted digitally until Oct. 28.

SECURE 2.0 Guidance Delays Catch-Up Contribution Limitations, Corrects Legislative Error. The Treasury Department and IRS issued temporary guidance (Notice 2023-62) on Aug. 25, providing a two-year “administrative transition period” for new requirements with respect to catch-up retirement-account contributions. Historically, taxpayers over age 50 were eligible to make additional contributions above annual limits to either traditional or Roth accounts within an employer-provided 401(k) plan. However, the SECURE 2.0 Act (Pub. L. 117-328) imposed new limitations requiring employees whose annual wages exceed $145,000 (inflation-adjusted) to make catch-up contributions only as post-tax Roth deferrals. While the provision was scheduled to apply in taxable years beginning after 2023, the temporary guidance delayed the limitations on high-income taxpayers until 2026. Regulators explained that the delay was intended to allow plan sponsors additional time to comply with the new rules.

The temporary guidance also corrects a drafting error embedded in SECURE 2.0 that would have inadvertently eliminated catch-up contributions entirely beginning in 2024. Although several Treasury Department officials had previously expressed skepticism over the agency’s ability to unilaterally fix Congress’ mistake, the guidance clarifies that the unintentional elimination of a tax code section “does not change [the ability for taxpayers to make catch-up contributions] for taxable years beginning after Dec. 31, 2023.” Lawmakers on both sides of the aisle had offered support for a year-end technical corrections bill to address the error, and a legislative solution may still be pursued if the Treasury Department’s authority to make the correction is questioned.

In addition to these clarifications, the notice asserts that further guidance will be issued to address several outstanding uncertainties, including the application of the rules to multiemployer retirement plans. The Treasury Department and IRS requested feedback with respect to the guidance or any other elements of the new catch-up-contribution rules by Oct. 24, 2023.

Regulators Issue Energy Guidance for Low-Income Bonus Credit Applicants, Federal Labor Guardrails for Tax Credits. Earlier this month, the Labor Department, Treasury Department and IRS finalized guidance for aspects of several clean-energy tax credits created or modified by the Inflation Reduction Act (IRA, Pub. L. 117-169). The guidance concerns the upcoming application process for the new section 48(e) Low-Income Communities Bonus Credit Program and the modified prevailing-wage and apprenticeship requirements associated with most of the energy production and investment tax credits.

The Treasury Department and IRS promulgated Final Regulations (TD 9979) and a Revenue Procedure (Rev. Proc. 2023-27) on Aug. 10 governing the allocation process with respect to the additional tax credits for up to 1.8 gigawatts of small solar and wind projects. Unlike most energy-tax incentives included in the IRA, the credit operates through a maximum allocation, so taxpayers must submit individual applications for consideration under a competitive-award process opening later this year. The final rules generally maintain provisions in earlier guidance, including the creation of two Additional Selection Criteria prioritizing projects owned by tribal or tax-exempt enterprises, as well as facilities located in Persistent Poverty Counties or census tracts designated by the Climate and Economic Justice Screening Tool.

The Labor Department Wage and Hour Division issued a Final Rule (RIN 1235-AA40) to amend the Davis-Bacon Act—significantly updating the labor laws for the first time in nearly 40 years. While the changes do not affect tax law directly, several tax provisions, including most of the energy credits, rely on the labor standards to impose guardrails for construction projects assisted by federal funding. The amended rules modify the process of determining the prevailing-wage rates for each geographic area, and they modernize the reporting and compliance requirements imposed on taxpayers and their subcontractors.

IRS Clarifies Rules for New Corporate AMT. On Sept. 12, the IRS issued Notice 2023-64, providing additional interim guidance that is intended to further clarify the application of the new corporate alternative minimum tax (CAMT), which was enacted pursuant to the Inflation Reduction Act of 2022. The Treasury Department and the IRS anticipate that forthcoming proposed regulations will provide rules that are consistent with the interim guidance. Specifically, the Notice describes rules for determining a taxpayer’s applicable financial statement and adjusted financial statement income (AFSI), including rules applicable to tax consolidated groups and certain foreign corporations. It provides rules for the AFSI adjustments for the depreciation of section 168 property, the amortization of qualified wireless spectrum, the treatment of certain taxes and the prevention of certain duplications and omissions. It also describes rules regarding the determination of applicable corporation status, the CAMT foreign tax credit and financial statement net operating losses. Finally, it provides a request for comments and the procedure for submitting such comments.

If you have questions about the CAMT, please reach out to a member of the Tax Policy Team.

At a Glance

Bipartisan Group of Senators Express Concern about Potentially Harmful Tax-Exempt Hospital Practices. On Monday, Aug. 7, Sens. Elizabeth Warren (D-MA), Raphael Warnock (D-GA), Bill Cassidy (R-LA) and Chuck Grassley (R-IA) wrote letters to IRS Commissioner Daniel Werfel, Tax Exempt and Government Entities (TE/GE) Commissioner Edward Killen, and Treasury Inspector General for Tax Administration (TIGTA) Commissioner J. Russell George accusing certain nonprofit hospitals of engaging in potentially harmful debt collection practices.

The bipartisan group of senators wrote that such hospitals were taking advantage of a broad definition of the term “community benefit” in IRS rules and redeeming tax exemptions for practices that are not contributing to reduced essential care costs for low-income consumers, contrary to the intention of the rules. The letter calls on the IRS and the TE/GE division to ensure standardization of nonprofit hospitals’ community benefit information, and to implement more rigorous reporting standards on IRS Form 990 and Schedule H. They also urged TIGTA to conduct audit reports to determine whether the IRS is ensuring that nonprofit hospitals comply with community benefits requirements, including whether any updates to Form 990 Schedule H effectively increase reporting transparency.

Ways and Means Committee Solicits Information about Relationship between Tax-Exempt 501 Organizations and Political Contributions. On Aug. 14, House Ways and Committee Chairman Jason Smith (R-MO) and Oversight Subcommittee Chairman David Schweikert (R-AZ) published a Request for Information (RFI) regarding the political activities of tax-exempt 501(c)(3) and 501(c)(4) organizations. They raise concerns that these organizations can operate as political action committees (PACs) and circumvent IRS scrutiny by donating to candidates running for political office, and that money flowing into such organizations may be originating from foreign sources, demonstrating that foreign interests could unduly influence U.S. elections. The RFI solicits stakeholders and the public to answer questions regarding the IRS’s current definition of “political campaign intervention” as it relates to 501(c)(3) and 501(c)(4) organizations and whether Congress and federal agencies should consider policies and actions mitigating the ability for foreign nationals to utilize tax-exempt organizations in contributing to political candidates.

FASB Approves Expanded Tax Disclosure and Transparency Requirements. The Financial Accounting Standards Board approved new requirements mandating companies to specifically delineate the amount of income taxes paid at the federal, state and local levels in annual financial reports. Previous rules only required that companies list the total amount of cash taxes paid. Supporters said that it would help increase transparency and help inform companies of risks and opportunities, while detractors argued that it would add to companies’ workload and may raise financial sensitivity issues. The rules will go into effect starting with 2025 annual reports.

Judge Rules in FTC’s Favor in Lawsuit Against Intuit’s TurboTax. Administrative Law Judge Michael Chappell ruled that Intuit was deceptively promoting its tax-preparation product, TurboTax, as free to consumers. The ruling would require Intuit to change its advertising methods for TurboTax, including specifically listing forms that qualify for TurboTax’s complimentary file option and specifying that most taxpayers would not qualify for free tax return preparation. An Intuit spokesperson denounced the decision as “[coming] from an FTC-employed judge in a case the FTC brought before itself” and is thus “flawed” and “groundless.” Intuit also said that it plans to appeal the ruling.

Senators Seek IRS Guidance on NIL Collectives. Sens. Ben Cardin (D-MD) and John Thune (R-SD) sent a letter to IRS Commissioner Daniel Werfel and Treasury Assistant Secretary for Tax Policy Lily Batchelder on July 31, requesting formal guidance on the taxable status of name, image and likeness (NIL) collectives. This follows a general legal advice memorandum released by the IRS in May that clarified that NIL collectives—organizations that fund and facilitate NIL deals for student-athletes—are generally not tax-exempt. The senators approved of the IRS’s conclusion and requested that it be adapted into more widely applicable guidance, such as a formal revenue ruling. The letter also highlighted the senators’ Athlete Opportunity and Taxpayer Integrity Act (S. 1454), which would eliminate tax deductions for compensation provided to athletes for NIL purposes.

Lawmakers Seek IRS Guidance on Historic Preservation Easements. A bipartisan group of House Ways and Means Committee members sent a letter to IRS Commissioner Daniel Werfel on Aug. 9 to “share suggestions to improve the recent proposed safe harbor guidance for the historic preservation community.” The letter states that historic preservation easement programs help to aid in the process of urban renewal and community revitalization, but that compliance and jurisdictional issues caused by a lack of IRS and Treasury guidance have made pursuit of such programs “prohibitive” and legally unclear. The letter urges Commissioner Werfel to provide clear guidance regarding the utilization of the historic preservation easement program.

IRS Issues Updated Guidance on R&D Expensing Reporting. On Sept. 8, the IRS issued Notice 2023-63, which provides interim guidance on Amortization of Specified Research or Experimental Procedures under Internal Revenue Code §174, the nonrefundable Research and Development (R&D) tax credit. Clarifications include identifying what costs can be amortized under the Tax Cuts and Jobs Act (TCJA, Pub. L. 115-97), guidance on short tax years, and a proposed amendment to the interpretation of accounting methods and cost sharing in certain contracts. Comments are due to the Treasury Department by Nov. 24.

Treasury Issues Roadmap on Clean Energy Tax Credits Guidance. Deputy Treasury Secretary Wally Adeyemo and Assistant Secretary for Tax Policy Lily Batchelder announced on Friday that the Treasury Department will begin to issue guidance on several energy and tax credits implemented as part of the Inflation Reduction Act (IRA, Pub. L. 117-169). Batchelder stated that the Treasury Department will first issue guidance on the energy efficient home credit and sustainable aviation fuel credit and will also plan to release guidance before the end of the year on the investment tax credit, the advanced manufacturing production tax credit, the electric vehicle credit provision for "foreign entities of concern" and clean hydrogen subsidies. The department previously missed a deadline on issuing guidance on the clean hydrogen credits.

Brownstein Bookshelf

Tax Foundation Pillar Two Report Counters JCT Study’s Findings. The nonpartisan Tax Foundation released a report discussing the potential consequences of a United States and international adoption of proposed OECD Pillar Two agreement. They found that, although the agreement may reduce the U.S. tax base and limit the tax-policy setting powers of Congress, foreign adoption of Pillar Two will have an estimated net increase of U.S. corporate tax revenues by $34.9 billion over 10 years; however, U.S. shareholders would experience lower post-corporate-tax incomes. This result contrasts with the Joint Committee on Taxation’s Pillar Two study released in June finding that the United States could stand to lose at least $56.5 billion with foreign adoption of Pillar Two.

IRS Releases 2024 Premium Tax Credit Percentage Tables. The IRS has issued indexing adjustments for calculating an individual’s premium tax credit amount under Internal Revenue Code §36B, for qualifying health insurance plans beginning in 2024.

Hearings and Events

House Ways and Means Committee

On Thursday, the full committee will hold a “Member Day” meeting, an opportunity for Ways and Means Committee members and stakeholders to promote legislation before the Ways and Means Committee.

Senate Finance Committee

On Thursday, the committee will hold a markup of the United States-Taiwan Expedited Double-Tax Relief Act.